Brand Copay: What It Is and How to Save on Prescription Costs

When you pick up a prescription, the amount you pay out of pocket is called your brand copay, the fixed amount you pay for a brand-name drug under your insurance plan. It's not the full price of the medicine—it's just your share, set by your insurer. But here’s the thing: brand copays are often way higher than what you’d pay for the generic version, even though both drugs work the same way. This isn’t a glitch—it’s how the system is built to push you toward cheaper options. Many people don’t realize that switching to a generic can cut their monthly drug bill by 80% or more. That’s not just savings—it’s life-changing for people managing chronic conditions like high blood pressure, diabetes, or depression.

Why do brand copays exist? Drug companies spend millions marketing their branded versions and patent them to block generics for years. Once that patent expires, other manufacturers can produce the same drug at a fraction of the cost. But your insurance plan might still charge you a high copay for the brand unless you first try the generic. That’s called step therapy, a process where insurers require you to try lower-cost alternatives before approving more expensive ones. It’s not always about cost—it’s about control. And if your doctor insists the brand is necessary, you can often appeal the decision. Many patients don’t know this is an option.

Then there’s drug affordability, the broader challenge of paying for prescriptions when income doesn’t match rising prices. Even with insurance, some brand copays hit $100 or more per month. For seniors on fixed incomes or young adults without coverage, that’s impossible. That’s why programs like prescription assistance, free or low-cost drug programs offered by manufacturers and nonprofits exist. Community clinics, patient advocacy groups, and even some pharmacies offer discounts or coupons that slash those copays down to $5 or $10. You don’t need to be poor to qualify—many programs just require proof of income or insurance status.

And it’s not just about the price tag. Sometimes the brand feels better—maybe it’s easier to swallow, or you’ve been on it for years and your body responds differently. But before you accept the higher copay without question, ask your pharmacist: "Is there a generic?" and "Can you check if my insurance will cover it at a lower cost?" Most of the time, the answer is yes. You’re not being difficult—you’re being smart.

Below, you’ll find real-world guides on how to cut prescription costs, understand insurance rules, and find help when you need it most. From how generic drugs are approved to where to get free medications, these posts give you the tools to stop overpaying—and start taking control of your health without breaking the bank.

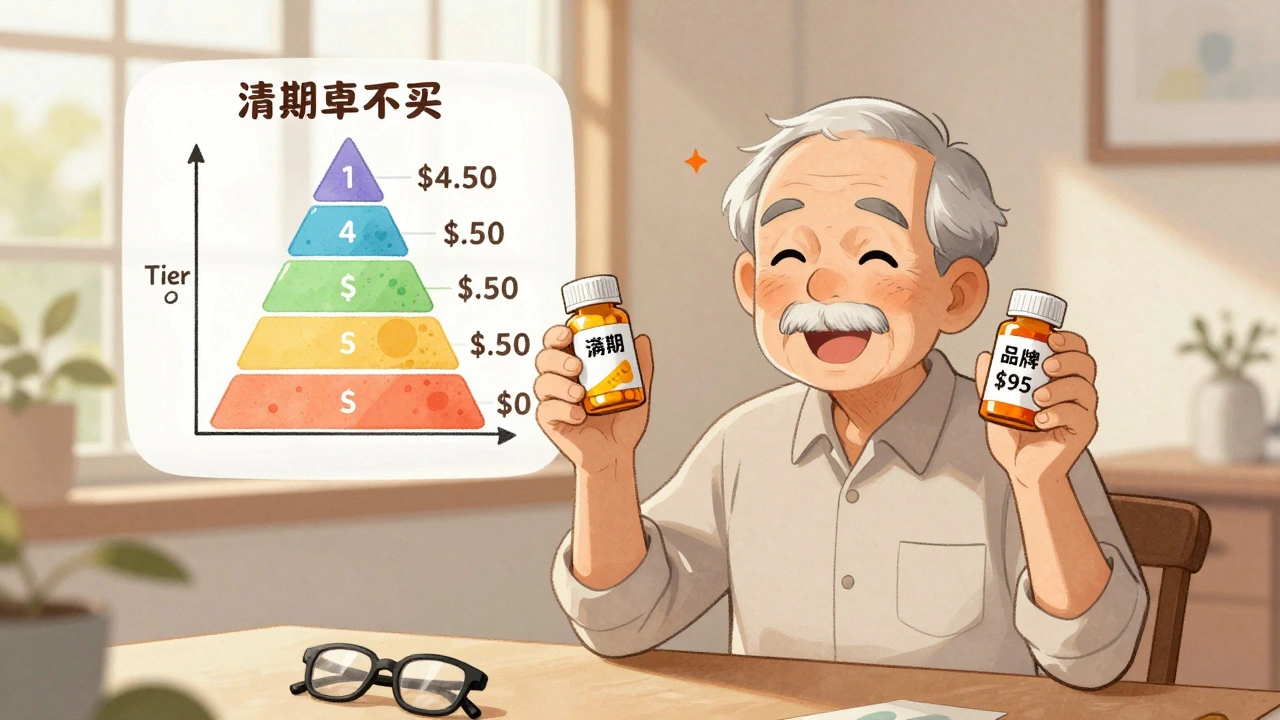

Generic Copays vs Brand Copays: Average 2024 Costs Explained

Learn the real costs of generic vs brand-name drug copays in 2024. See how Medicare and private plans charge differently, what’s changing in 2025, and how to save money on prescriptions.

Detail