When you pick up a prescription, the price you pay at the pharmacy isn’t the full cost of the drug. It’s your copay - the portion you cover out of pocket. But here’s the thing: if you’re taking a generic drug, you might pay $5. If you’re taking the brand-name version of the same medicine, you could pay $100 or more. That’s not a mistake. It’s by design.

Why Generic and Brand Copays Are So Different

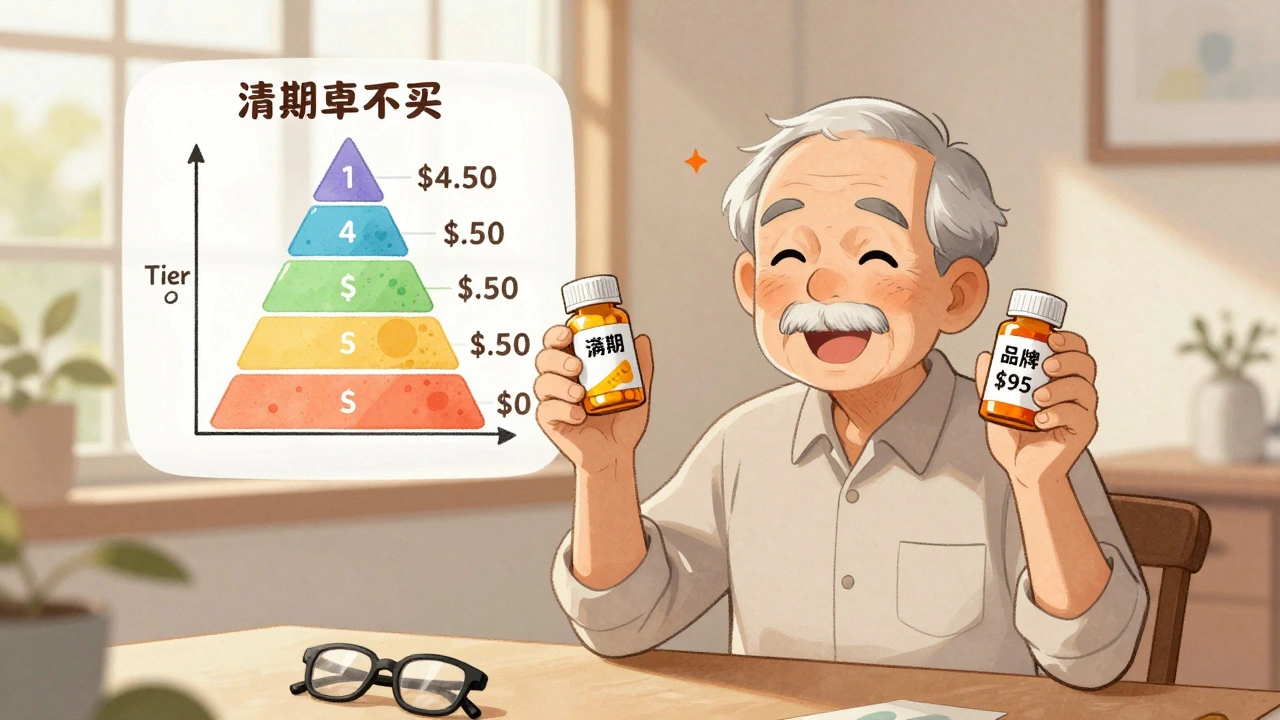

The difference between generic and brand copays isn’t random. It’s built into how insurance plans work. Since 2006, Medicare Part D and most private insurance plans have used a tiered system to encourage people to choose cheaper, equally effective generic drugs. The idea is simple: make generics easy and affordable, and make brand-name drugs more expensive unless there’s a real medical reason to use them. In 2024, most plans have four tiers:- Tier 1: Preferred Generic - Usually $0 to $10

- Tier 2: Non-Preferred Generic - Around $7 to $15

- Tier 3: Preferred Brand - Median $47

- Tier 4: Non-Preferred Brand - Median $100

Medicare Advantage vs Standalone Drug Plans

Not all plans work the same way. If you’re on a Medicare Advantage Prescription Drug (MA-PD) plan - which about 45% of Medicare beneficiaries use - you’re likely paying fixed copays. That means you know exactly what you’ll pay each time: $5 for a generic, $47 for a preferred brand. But if you’re on a standalone Prescription Drug Plan (PDP), you’re more likely to pay coinsurance - a percentage of the drug’s total cost. That can be a problem. If your brand-name drug costs $300, and your plan charges 22% coinsurance, you pay $66. But if that same drug jumps to $450 next month? Your copay goes up too. No warning. No cap. Just a higher bill. For non-preferred brand drugs, the difference gets even starker. In MA-PD plans, 94% of enrollees pay a flat $100 copay. In PDPs, nearly 80% pay 47% of the drug’s price - which could mean $150, $200, or more if the drug is expensive.What Happens When You Choose a Brand Over a Generic

Some doctors write prescriptions for brand-name drugs because they think they’re better. Sometimes, they’re right - but often, they’re not. If your doctor writes “dispense as written,” your plan still has rules. Many plans have a policy called “Member Pay the Difference.” Here’s how it works: If there’s a generic version available, and you choose the brand anyway, you pay your normal copay - plus the full price difference between the generic and the brand. So if the generic costs $5 and the brand costs $95, you pay $5 (your copay) + $90 (the difference) = $95. That’s not a mistake. That’s the plan’s way of saying, “We’re not paying extra for this.” One Medicare beneficiary in Florida reported paying $95 for a 90-day supply of a brand-name drug that had a $15 generic alternative. His doctor wouldn’t switch him because of side effects - but he didn’t know his plan would charge him $80 extra just for choosing the brand. He ended up paying $1,140 a year for a drug that could’ve cost $180 with the generic.

Specialty Drugs Are a Whole Other Level

If you’re taking a drug for cancer, MS, or rheumatoid arthritis, you’re probably on Tier 5 - the specialty tier. These drugs can cost thousands. Copays here aren’t fixed. They’re often percentage-based: 33% of the drug’s cost, up to $5,000, then 15% after that. One 60-day supply of a specialty drug might cost $150 out of pocket. Another could cost $3,000. It all depends on the drug, the plan, and whether it’s on your plan’s preferred list. And yes - there are often prior authorization requirements. Your doctor has to prove you’ve tried cheaper options first. That’s called step therapy. It’s frustrating, but it’s standard.Extra Help? Lower Copays for Low-Income Beneficiaries

If your income is limited, you might qualify for Medicare’s Extra Help program. In 2024, this program capped copays at $4.50 for generics and $11.20 for brand-name drugs - no matter what your plan says. That’s a huge relief for people living on fixed incomes. But here’s the catch: You have to apply. Many people don’t know they qualify. The Social Security Administration estimates that nearly 40% of people who are eligible for Extra Help never sign up. If you’re paying more than $10 for a generic or $20 for a brand, it’s worth checking if you qualify.What’s Changing in 2025

The Inflation Reduction Act didn’t just tweak the system - it changed it. Starting January 1, 2025, there’s a new rule: no one pays more than $2,000 a year out of pocket for prescription drugs, no matter how many brand-name drugs they take. That’s a big deal. Right now, someone taking a $100-a-month brand drug could easily hit $1,200 in out-of-pocket costs before reaching catastrophic coverage. In 2025, they’ll pay $2,000 total - and then the plan covers the rest. For people on multiple expensive drugs, this could mean saving thousands. Also, 98% of Medicare Part D plans in 2025 will offer $0 copays for preferred generics. That’s up from 87% in 2024. Insulin is already capped at $35 a month - and that cap applies to both generic and brand insulin.

How to Find Your Real Costs

You can’t guess your drug costs. You have to check. Every year, by October 15, your plan must publish its formulary - the list of drugs it covers and how much you’ll pay for each. Use the Medicare Plan Finder tool. Enter your exact medications, your zip code, and your preferred pharmacy. It will show you the exact copay for each plan. Don’t just look at the monthly premium. Look at your annual drug costs. A plan with a $10 premium but $100 brand copays could cost you $1,200 a year for one drug. A plan with a $50 premium but $40 brand copays might cost only $480. That’s a $720 difference.What to Do If You Can’t Afford Your Meds

If you’re struggling to pay:- Ask your doctor if there’s a generic or preferred brand alternative.

- Ask if you qualify for Extra Help or manufacturer patient assistance programs.

- Check if your pharmacy offers cash prices - sometimes, paying out of pocket without insurance is cheaper than using your copay.

- Call your plan’s customer service. Ask: “Is there a therapeutic alternative on a lower tier?”

Saurabh Tiwari

December 1, 2025 AT 16:34bro i just found out my $90 monthly brand med has a $5 generic and i’ve been paying extra for nothing for 2 years 😭

my doc never mentioned it and my plan didn’t flag it

now i’m switching and saving $1k a year

why is this not common knowledge??

also why do we even have brand names if they’re just the same pills with a fancy label?? 🤡

Shubham Pandey

December 2, 2025 AT 09:35generic = same stuff cheaper

Girish Padia

December 3, 2025 AT 09:08people who choose brand over generic are just being lazy or listening to pharma ads

you think your body needs the ‘real’ version? nah

it’s the same molecule, same FDA approval, same side effects

you’re just paying for marketing and a prettier bottle

and then you wonder why healthcare costs are insane

stop being a sucker

Chris Wallace

December 4, 2025 AT 04:32I’ve been on a few different Medicare plans over the last decade and this tiered system is honestly one of the few things that actually works well-if you know how to navigate it.

But the problem isn’t the structure, it’s the lack of transparency. Most people don’t realize their plan’s formulary changes every year, or that a drug they’ve been on for years could suddenly jump from Tier 1 to Tier 4 without warning.

I spent months trying to figure out why my copay went from $10 to $89 one month. Turns out the generic switched from one manufacturer to another, and the new one wasn’t ‘preferred’ anymore. No email. No notice. Just a surprise at the pharmacy counter.

And the coinsurance trap for PDPs? That’s a nightmare. One month your drug costs $200, next month it’s $350 because of a ‘supply issue’-and suddenly you’re paying $77 instead of $44. No cap. No explanation.

I get why plans do it-to push people toward generics-but they need to make the rules clearer. People aren’t trying to game the system. They’re just trying to stay alive.

John Webber

December 5, 2025 AT 08:10why do u pay 100$ for a pill??

generic is 5$ and does the same thing

my uncle takes the brand and says he feels better but i think its placebo

also extra help is free money if u qualify

why dont more people apply??

so many ppl are strugglin and dont even know

Elizabeth Farrell

December 6, 2025 AT 01:11Thank you for writing this. As someone who helps elderly relatives navigate Medicare, I see this confusion every single day.

Many of them don’t understand why their copay went from $12 to $98 overnight. They think the medicine changed. They don’t realize it’s the plan’s formulary update. They panic. They skip doses. Some even stop taking them.

The Extra Help program is a lifeline-but it’s buried in paperwork and confusing websites. I’ve helped three people apply this year. All of them were shocked to find out they qualified. One was paying $200/month for a drug that now costs $11.20.

If you’re over 65 and paying more than $15 for a generic, please, please, please check Extra Help. It’s not just for the poorest-it’s for anyone under 150% of the federal poverty level. That’s more people than you think.

And if you’re a caregiver? Print out the Medicare Plan Finder guide. Keep it next to the pill organizer. This stuff matters.

Saket Modi

December 6, 2025 AT 14:37why is this even a thing

we pay 5$ for generic and 100$ for brand

the pills are the same

pharma companies are literally just charging us for the logo

and doctors just keep writing the brand name like they’re getting kickbacks

and we sit there paying like idiots

why is this legal??

also i just got a $120 bill for a drug that’s $8 generic

my plan didn’t tell me

so now i’m mad and broke

alaa ismail

December 8, 2025 AT 04:58just switched my dad from brand to generic for his blood pressure med

same results, $5 instead of $95

he didn’t even notice

but his wallet did

also found out he qualified for Extra Help

got his copays cut to $4.50

took me 20 mins on the SSA website

why does no one talk about this??

also 2025’s $2k cap is gonna be a game changer

finally someone’s listening